May 2023 Commentary

May 05, 2023

Market Recap

Stocks and bonds experienced some choppiness but finished higher in April. The stock market, as measured by the S&P 500, was up 1.6%, but the market’s advance is becoming narrower, where fewer stocks are participating in the upward movement. Lower market cap indices, such as the S&P Small Cap and Mid Cap indices were down 2.9% and 0.5% for the month, respectively. This suggests that the underlying foundation of the market may not be as strong as it seems by just looking at the S&P 500. In the table below, note the disparity in year to date performance between large caps and small to mid-cap stocks.

- The regional banking crisis persists, as we continue to witness additional bank failures.

- Fed policy goals remain the same, but data suggests we could be nearing an end to this tightening cycle.

- Inflation continues to fall, but we remain far away from the Fed’s long-term target.

- The need to raise the debt ceiling has been an issue for several months now, but we are getting close to crunch time and need a resolution.

- The liquidity backdrop of the economy and the markets is tight with money supply contracting, the implementation of quantitative tightening, and the reduction of bank lending.

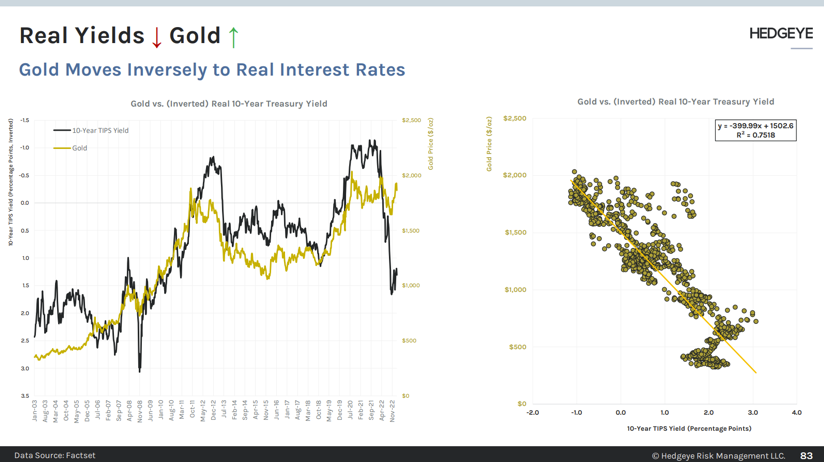

- Gold continues to move higher with a favorable backdrop.

US Economic Growth

While the U.S. economy did manage to grow in the first quarter at a rate of 1.1%, the rate of growth did not meet the forecasted rate of 2% growth, and it also represents a continued pattern of softening. Given the impact of higher rates, softening consumer spending, and the credit crunch from the tightening of lending standards with banks, the U.S. economy is likely at an inflection point of potentially tipping into a recession.

Regional Banks Remain Under Pressure

First Republic Bank was taken into receivership by the FDIC and then sold to J.P. Morgan Chase shortly thereafter. The news further fuels uncertainty in the regional banking sector and exacerbates the current credit crunch. Further, on May 3rd, it was announced that PacWest Bancorp would be exploring several strategic options, including a sale of the bank. While the chapter has not fully played out, the company’s stock has plummeted 90% since March 8th, the inception of the banking crisis. The current situation is a manifestation of a post-pandemic monetary policy bubble, where banks and other market participants seized on the low cost of capital to take on risk.

Fed Policy and Inflation

Nothing has changed as of yet with respect to the Fed’s policy goal of 2% long-term inflation, however, we may be near the end of Fed’s rate hiking regime. In the May 3rd policy meeting, the Fed did implement the anticipated 25 basis point rate hike but softened their tone about future rate hikes. However, there are no guarantees that this will be the final increase with the inflation rate still around 5% and labor markets remaining tight/strong. Assuming no further rate hikes, we expect that the Fed funds rate will remain elevated through the end of 2023 and possibly into the early part of next year.

As we await the April inflation numbers, the core inflation rate is still running around 5.5%, well above the Fed’s long term target. With housing and wage inflation remaining sticky, Fed policy makers may find it challenging to recommend lowering rates in their effort to curtail inflation and reverse the effects of the post-pandemic liquidity bubble.

Debt-Ceiling Debate

Discussions to raise the debt ceiling are ongoing. Most agree that the issue will be resolved, but not without some in fighting between the political parties, which can cause some angst for the markets in the short term. The House passed a bill to raise the debt-ceiling by $1.5 trillion, in exchange for $4.5 trillion of spending cuts over time. While this proposal is likely a bridge too far for the Senate and Administration, it does formally kick off meaningful negotiations to reach a compromise.

While resolving the issue is critical to the functioning of our government, equally important are the implications once the ceiling has been raised. The Treasury will likely begin to issue a significant amount of debt to support the finances of the government and to repay monies that have been spent from the Treasury General account to fund the government ahead of raising the ceiling. This Treasury bond issuance will most likely serve as another form of tightening monetary policy and reduce financial markets liquidity which could be an additional headwind for the domestic economy.

Financial Markets Liquidity

M2 – money supply continues to contract, demonstrating the largest negative year-over-year growth rate since 1980. Supply contractions are rare, with this round being driven by the financial system shedding excesses from the post-pandemic stimulus. Further, we continue to see tight credit conditions and reduction in lending emanating from the regional banking issues, as well as the continued quantitative tightening. The combined effect of these will serve as a stiff headwind for our economy and financial markets liquidity for 2023.

Gold Continues to Shine

The combination of recession fears, a falling inflation rate, and lower long-term bond yields has sent gold jumping higher, up roughly 9% year to date. While many other industrial commodities have been crashing in price, precious metals, gold in particular, have been performing well. Gold tends to perform well during times of economic stress and falling inflation and move inversely to interest rates.

The Bottom Line

While the S&P has held up rather well this year given the recent banking turmoil and recession fears, more uncertainty lingers ahead related to when the Fed will change course and whether corporate earnings will be able to hold up to expectations. We believe that the apparent strength of the S&P 500 is being bolstered by only a few larger constituents, such as Meta Platforms, Nvidia, Apple, and Microsoft, which may be masking underlying weakness in the broader market. At the same time, the S&P 500 is trading at a valuation more closely correlated with mid-teens earnings growth, whereas earnings growth is likely to be negative this year. As such, the S&P 500 currently seems to be pricing in a fair amount of good news and a higher probability of a soft-landing for the U.S. economy. Such a soft-landing scenario would be supported by a resilient labor and housing market, along with continued strength in the services sector of the economy.

Our cautionary tone is reflective of how we are currently managing our client portfolios. While we build our portfolios based upon client objectives and with a focus on long-term investment performance, currently, we do have our portfolios positioned conservatively with equities at the low end of our allocation range and further conservative positioning within our equity sleeve. Furthermore, we maintain exposures to alternative asset classes, such as gold and private credit, that tend to be less correlated with the stock market, and in some cases, perform well in times of market stress. Lastly, with a likely peak in inflation and the likely waning of the current rate hike cycle by the Fed, the bond component of our portfolios should perform better and serve as a ballast against any stock market weakness.

Disclosures

Important Information

Investment Advisory services are provided through Bison Wealth, LLC located at 3550 Lenox Road NE Suite 2550 Atlanta, GA 30326. Securities are offered through Metric Financial, LLC. located at 725 Ponce de Leon Ave. NE Atlanta, GA 30306, member FINRA and SIPC. Bison Wealth is not affiliated with Metric Financial, LLC., More information about the firm and its fees can be found in its Form ADV Part 2, which is available upon request by calling 404-841-2224. Bison Wealth is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training.

The statements contained herein are based upon the opinions of Bison Wealth, LLC (“Bison”) and the data available at the time of publication and are subject to change at any time without notice. This communication does not constitute investment advice and is for informational purposes only, is not intended to meet the objectives or suitability requirements of any specific individual or account, and does not provide a guarantee that the investment objective of any model will be met. An investor should assess his/ her own investment needs based on his/her own financial circumstances and investment objectives. Neither the information nor any opinions expressed herein should be construed as a solicitation or a recommendation by Bison or its affiliates to buy or sell any securities or investments or hire any specific manager. Bison prepared this Update utilizing information from a variety of sources that it believes to be reliable. It is important to remember that there are risks inherent in any investment and that there is no assurance that any investment, asset class, style or index will provide positive performance over time. Diversification and strategic asset allocation do not guarantee a profit or protect against a loss in a declining markets. Past performance is not a guarantee of future results. All investments are subject to risk, including the loss of principal.

Index definitions: “U.S. Large Cap” represented by the S&P 500 Index. “U.S. Small Cap” represented by the S&P 600 Index. “International” represented by the MSCI Europe, Australasia, Far East (EAFE) Net Return Index. “Emerging” represented by the MSCI Emerging Markets Net Return Index. “U.S. Aggregate” represented by the Bloomberg U.S. Aggregate Bond Index. “Treasuries” represented by the Bloomberg U.S. Treasury Bond Index. “Short Term Bond” represented by the Bloomberg 1-5 year gov/credit Index. “U.S. High Yield” represented by the Bloomberg U.S. Corporate High Yield Index. “Real Estate” represented by the Dow Jones REIT Index. “Gold” represented by the LBMA Gold Price Index. “Bitcoin” represented by the Bitcoin Galaxy Index.

- June 2026 (2)

- April 2026 (1)

- March 2026 (1)

- February 2026 (1)

- January 2026 (1)

- December 2025 (3)

- September 2025 (1)

- August 2025 (1)

- July 2025 (1)

- June 2025 (1)

- May 2025 (1)

- April 2025 (1)

- March 2025 (2)

- January 2025 (5)

- August 2024 (8)

- July 2024 (1)

- June 2024 (1)

- May 2024 (1)

- April 2024 (1)

- March 2024 (1)

- February 2024 (2)

- January 2024 (3)

- December 2023 (1)

- November 2023 (1)

- October 2023 (1)

- September 2023 (1)

- August 2023 (1)

- July 2023 (1)

- June 2023 (1)

- May 2023 (1)

- April 2023 (1)

- March 2023 (1)

- February 2023 (1)

- January 2023 (1)

- December 2022 (1)

- November 2022 (1)

- October 2022 (1)

- September 2022 (1)

- August 2022 (1)

- July 2022 (1)

- May 2022 (3)