Share this

Feb 07, 2023

January 2023 Market Recap

We kicked off the New Year with a nice rally in the financial markets across most asset categories, including stocks, bonds, gold and precious metals, and international stocks (both developed and emerging markets). Let’s review the performance of our key market barometers for the month of January.

While we saw solid broad-based stock performance in January, the strongest performance was witnessed among those subsets or groups that were hit the hardest in 2022. For instance, compared to the S&P 500 return of 6.3% in January:

- “Profitless technology companies” were up 21%

- High beta stocks outperformed low beta stocks, up 15.2% vs 0.2%

- High Short Interest stocks outperformed low short interest, up 12.4% vs 3.7%

- Low dividend stocks outperformed high dividend stocks, up 12.2% vs 6.0%

- Small Caps outperformed large caps, up 9.5% vs 6.3%

- Bitcoin was up 39%, after being down 64% in 2022

By all accounts, January was a “risk-on” type of market, which leads to the logical question as to whether this rebound in “risk-on” assets is sustainable and represents the start of a new bull market, a rally within the same 2022 bear market similar to what we witnessed last June thru mid-August, or just part of an ongoing bottoming process for US stocks. Here is a summary of our thoughts on the economy and financial markets:

- Most economic data continues to indicate weakness and increasing potential for recession

- Consumer spending has been strong but continues to moderate

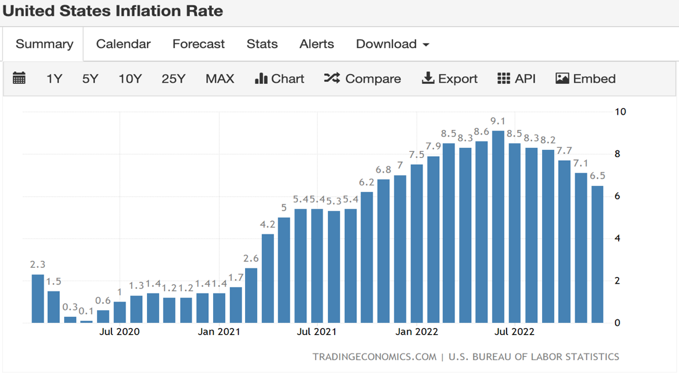

- Inflation continues to come down slowly, but the labor market is demonstrating surprising strength, adding fuel to the argument that the FED will maintain its hawkish posture for longer

- Debate over raising the debt ceiling is likely to dominate market headlines over the next several months, as the Treasury funds current spending from the Treasury General Account, since they are unable to issue new debt until the debt ceiling is raised

- The earnings reporting season kicked off in January, and it appears that the much anticipated corporate profits recession is upon us

Economy Continues to Weaken, Along with the US Consumer

The cumulative impact of rate hikes by the FED is continuing to have the desired effect of slowing the economy. The Institute for Supply Management (ISM) surveys, often seen as key leading indicators of economic activity, weakened further in December, while the non-manufacturing (services) segment sent a mixed signal with a positive reversal and uptick in January. Meanwhile, the ISM Manufacturing and New Orders surveys demonstrated continued deterioration falling further below the 50 level, indicating future economic contraction. GDP for the fourth quarter of 2022 came in at 2.9%, a modest slowdown from the 3.2% rate in the third quarter, driven by an increase in inventories.

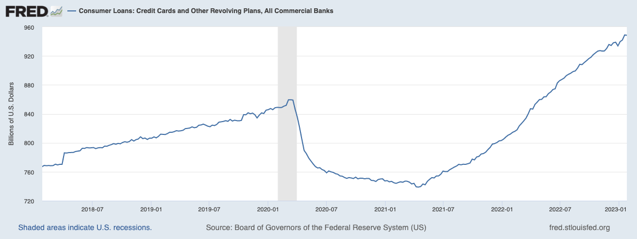

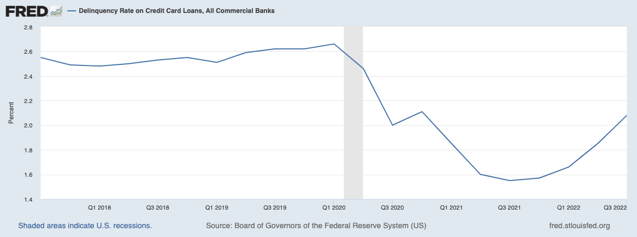

The consumer had been a bright spot helping to sustain economic growth in the fourth quarter. There are indications that the consumer may be under a bit of duress, given the rapid growth in consumer credit and the steep decline in the personal savings rate over the last several months. Further, while consumer credit delinquencies are still low, we are seeing the delinquency rates increase (a sign of stress to watch). Lastly, Amazon, an important barometer for retail consumer spending, guided down their consensus revenue forecast for the first quarter of 2023.

Inflation Moderates

The rate of inflation continued to decelerate coming in at 6.50% for December, a welcome sign for longer-term interest rates and the bond markets. With the supply chain issues subsiding and inventory levels increasing, we are seeing less pressure on prices, though we are carefully monitoring the labor market and wage pressures for a check on how hawkish the FED will remain through the year. On February 1st, the FED did reduce its most recent increase in the fed funds rate to 25 basis points (from 50), but it did not change its target rate of 5% nor its tone of hawkishness to bring the inflation rate down further.

The Debt-Ceiling Debate

Taking center stage in the news is the negotiations between the House of Representatives and the Executive Branch with respect to increasing the debt ceiling to be able to continue to fund the current government spending budget. Putting it simply, the Treasury needs to fund the government, but they cannot issue new debt for those expenses until the debt ceiling has been raised. The Treasury must drain its general checking account at the FED to fund day-to-day obligations. In effect, this is a direct liquidity injection of approximately $110B per month into the economy, essentially a form of quantitative easing from the Treasury that will continue to support financial system liquidity until the debt ceiling issue is resolved. Once the debt ceiling is raised, the Treasury will begin bond issuance again to fund the government operations and to repay the Treasury’s General Account. Opinions vary with respect to how this may impact the financial markets, but the last time this occurred was in the middle of 2011, which did lead to a significant correction in the stock market.

The Early Read on Corporate Earnings

To this point in time, almost half of S&P 500 companies have reported fourth quarter earnings. The average sales growth has been roughly 5% and earnings growth has come in at -3%. So, we are beginning to see the broad decline in corporate profits and reductions in earnings estimates for 2023. Based upon previous bear markets and recessions in the past, there may be further risk to profits, the potential for a profits recession, and a reduction in estimated corporate earnings for 2023. Will the markets look past negative earnings growth rates and the downward estimate revision cycle for corporate earnings? It remains to be seen as to whether the stock market has discounted trough earnings and is more focused on the potential easing of FED policy later in the year or early 2024.

The Bottom-Line

The growth outlook for the US economy is tepid at best, but in contrast with 2022, we expect the FED and global monetary policymakers to acknowledge the economic slowdown as the year progresses, resulting in a more stable monetary policy. This should reduce interest-rate volatility and asset price volatility as we head toward the 2nd half of 2023. While it is likely that the ride will remain bumpy at least for the first few months of the year, the overall outlook for both the stock and bond markets has improved in the last few months.

Stocks and bonds both had a great start to the year. Given the fact that the economic slowdown is in progress and the rate of inflation is indeed moderating, we are more constructive on the fixed-income market, favoring higher quality bonds. The S&P 500 has now rallied approximately 17% off its October lows, very similar to the rally witnessed into mid-August of 2022. We reiterate that the bottoming process for a bear market can take time. As such, we continue to maintain a conservative posture towards equities in our portfolios following this recent rally that was fueled by lower quality and higher beta companies. Nevertheless, we will continue to monitor and evaluate the relevant datapoints as it relates inflation, the economy, the FED, and corporate earnings as the year progresses to determine when to become more constructive on equities.

Disclosures

Important Information

Investment Advisory services are provided through Bison Wealth, LLC located at 3550 Lenox Road NE Suite 2550 Atlanta, GA 30326. Securities are offered through Metric Financial, LLC. located at 725 Ponce de Leon Ave. NE Atlanta, GA 30306, member FINRA and SIPC. Bison Wealth is not affiliated with Metric Financial, LLC., More information about the firm and its fees can be found in its Form ADV Part 2, which is available upon request by calling 404-841-2224. Bison Wealth is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training.

The statements contained herein are based upon the opinions of Bison Wealth, LLC (Bison) and the data available at the time of publication and are subject to change at any time without notice. This communication does not constitute investment advice and is for informational purposes only, is not intended to meet the objectives or suitability requirements of any specific individual or account, and does not provide a guarantee that the investment objective of any model will be met. An investor should assess his/ her own investment needs based on his/her own financial circumstances and investment objectives. Neither the information nor any opinions expressed herein should be construed as a solicitation or a recommendation by Bison or its affiliates to buy or sell any securities or investments or hire any specific manager. Bison prepared this Update utilizing information from a variety of sources that it believes to be reliable. It is important to remember that there are risks inherent in any investment and that there is no assurance that any investment, asset class, style or index will provide positive performance over time. Diversification and strategic asset allocation do not guarantee a profit or protect against a loss in a declining markets. Past performance is not a guarantee of future results. All investments are subject to risk, including the loss of principal.

Index definitions: “U.S. Large Cap” represented by the S&P 500 Index. “U.S. Small Cap” represented by the S&P 600 Index. “International” represented by the MSCI Europe, Australasia, Far East (EAFE) Net Return Index. “Emerging” represented by the MSCI Emerging Markets Net Return Index. “U.S. Aggregate” represented by the Bloomberg U.S. Aggregate Bond Index. “Treasuries” represented by the Bloomberg U.S. Treasury Bond Index. “Short Term Bond” represented by the Bloomberg 1-5 year gov/credit Index. “U.S. High Yield” represented by the Bloomberg U.S. Corporate High Yield Index. “Real Estate” represented by the Dow Jones REIT Index. “Gold” represented by the LBMA Gold Price Index. “Bitcoin” represented by the Bitcoin Galaxy Index.